Crash Course: Trump’s IRS Lawsuit Settlement

Trump got no payout—but he may have gotten something much more valuable

The Trump administration just settled Trump’s $10 billion lawsuit against the IRS. That sentence is already strange enough.

But the headline beneath the headline is even stranger. As part of the settlement, the Justice Department issued an order that appears to block the IRS from auditing President Trump, his family, his trusts, and affiliated companies for any tax returns filed before the May 2026 settlement date.

That is the part worth understanding.

What happened?

Trump sued the IRS and Treasury Department for $10 billion (yes, billion with a B) after a former IRS contractor leaked private tax information to the press. That leak was illegal, and the leaker was sentenced to five years in prison. Tax records are supposed to be confidential, and the government has a real obligation to protect them.

So, at one level, the lawsuit had a legitimate starting point in that the IRS failed to protect private taxpayer information.

But the settlement went much further than an apology for the leak.

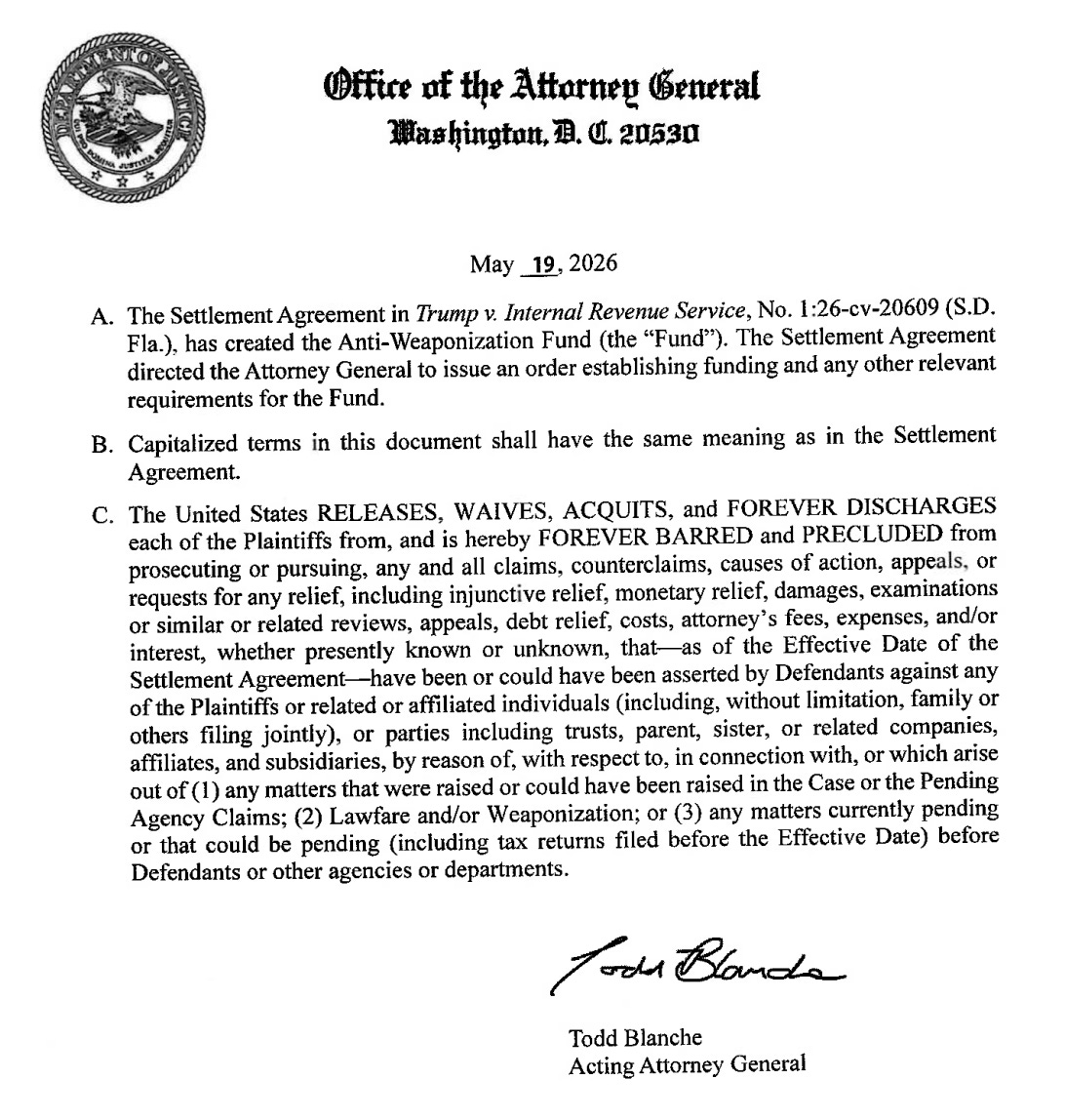

The agreement included no direct payment to Trump. Instead, the government apologized and agreed to dismiss the dispute. Then came the separate DOJ order, signed by Acting Attorney General Todd Blanche, that said the United States is “forever barred and precluded” from pursuing certain claims, reviews, or “examinations” involving Trump and related people or entities for tax returns filed before the settlement date.

In normal English: the deal blocks the IRS from auditing Trump-world tax filings from before May 18, 2026.

Why is that a big deal?

Because this is not how tax enforcement normally works.

The IRS can choose not to audit a return. It can finish an audit and find nothing. It can decide that the statute of limitations has expired. Those are all normal parts of tax administration.

But presidential audits are different.

Since the post-Watergate era, the IRS has had internal procedures saying that the individual income tax returns of the president and vice president are subject to mandatory examination. The point is simple—no IRS official should have to decide whether auditing the president is politically awkward. It should be automatic.

That system was supposed to protect everyone.

It protects the public by making sure the most powerful elected officials are following the same tax laws as everyone else. It protects the IRS by turning the audit into routine procedure instead of a political judgment call. And, in theory, it protects presidents by preventing accusations that the agency is targeting them for partisan reasons.

But the new order throws this long standing precedent out the window.

This is the Justice Department saying, in advance, that the IRS cannot audit a broad category of Trump-related past returns at all.

And it does not just cover Trump personally. The order extends to family members, trusts, companies, affiliates, subsidiaries, and related entities. In other words: a very large Trump-world umbrella.

That is why critics see this as more than a private legal settlement. They see it as political protection from future tax scrutiny.

Is this legal?

That is likely to be challenged.

The Justice Department can settle lawsuits, yes even with the sitting president of the United States. But whether it can use a settlement to bind the IRS this broadly is a serious question. Tax enforcement is supposed to follow ordinary legal procedures, not political bargaining.

There is also the obvious conflict concern. Trump leads the executive branch. The IRS, Treasury, and DOJ are all inside that branch. And Blanche, who signed the order, previously served as Trump’s personal attorney.

That does not automatically make the order invalid. But it makes the arrangement look exactly like the kind of thing independent tax enforcement is supposed to prevent.

The bottom line

The leak of Trump’s tax information was wrong.

But the remedy may be more troubling than the original violation.

The issue is not whether Trump deserved privacy. He did. The issue is whether a president’s own administration can shield him, his family, and his businesses from IRS scrutiny of past tax returns.

Because once tax enforcement can be turned off for the powerful, the problem is no longer just about taxes.